Sovereign Industrialisation - Silicon Roundabout Ventures, Feb 2026 Bulletin

Our "Build in Public" LP update, with fresh fund highlights, community events, and deeptech market insights. Written by our AI. Edited by our humans.

In This Edition

Sovereign Industrialisation: 🏛️ The 2026 deeptech inflection — from discovery phase to execution and sovereignty; quantum networking; sovereign defence; AI’s energy and security crisis; industrial scale-up.

Events: Dragon Chasers OG, Montenegro — 12–15 May.

GP Update: 8 companies above $1M revenue; patience in deeptech and the Fund II trajectory.

LP Private section: Co-investment Opportunities and Financial Update

A reminder of what we are about

Silicon Roundabout Ventures is a SuperAngel Seed fund in the UK investing in European Deep Tech startups. It leverages their community of 15,000 entrepreneurs and engineers, through which the team previously attracted, selected and helped launch 33 Deep Tech and Big Data startups now valued at over £6 Billion.

The fund is backed by top-tier VC Molten Ventures (LSE:GROW) and exited founders, engineers and execs: including ex googlers, amazonians and from 4 unicorns.

Thanks for reading Silicon Roundabout Ventures Community! Subscribe for free to receive new posts and support my work.

📅 Upcoming Events and Community Updates

Francesco will be at Dragon Chasers OG, Montenegro - 12th to 15th May 2026. If you’re an LP and might like to attend, reach out to us!

Portfolio Updates & Public Announcements

Our public portfolio tracker: https://siliconroundabout.ventures/portfolio

Leveraging our community to spot the very best of Europe’s talents before they go “global”, and write that super-early cheque that fuels their launch.

➕ New Announcements

No new announcements.

Performance Snapshot

Note: We do not book non-priced rounds as markups.

Silicon Roundabout Ventures LP II

Stay tuned for updates :)

Silicon Roundabout Ventures LP

Vintage: 2023 / Investments: 21 (closed)

Key Deeptech Areas: Future of Computing, Energy, and Defence

Fund Size: £5M

GP’s Angel Portfolio

Vintage: 2020 / Investments: 17

TVPI: 2X / DPI: 0.1X

Highlight Companies: Ori.co, Aegieq.com, Kaizan.ai, Nanusens.com, rnwl.co.uk, Ecosync, Axiom.ai

Community “Virtual” Portfolio

Vintage: 2016 / Companies considered: 26

Method for selection: Silicon Roundabout community pitch winners until the beginning of the GP investment activity

Simulated TVPI: 6-6.9X

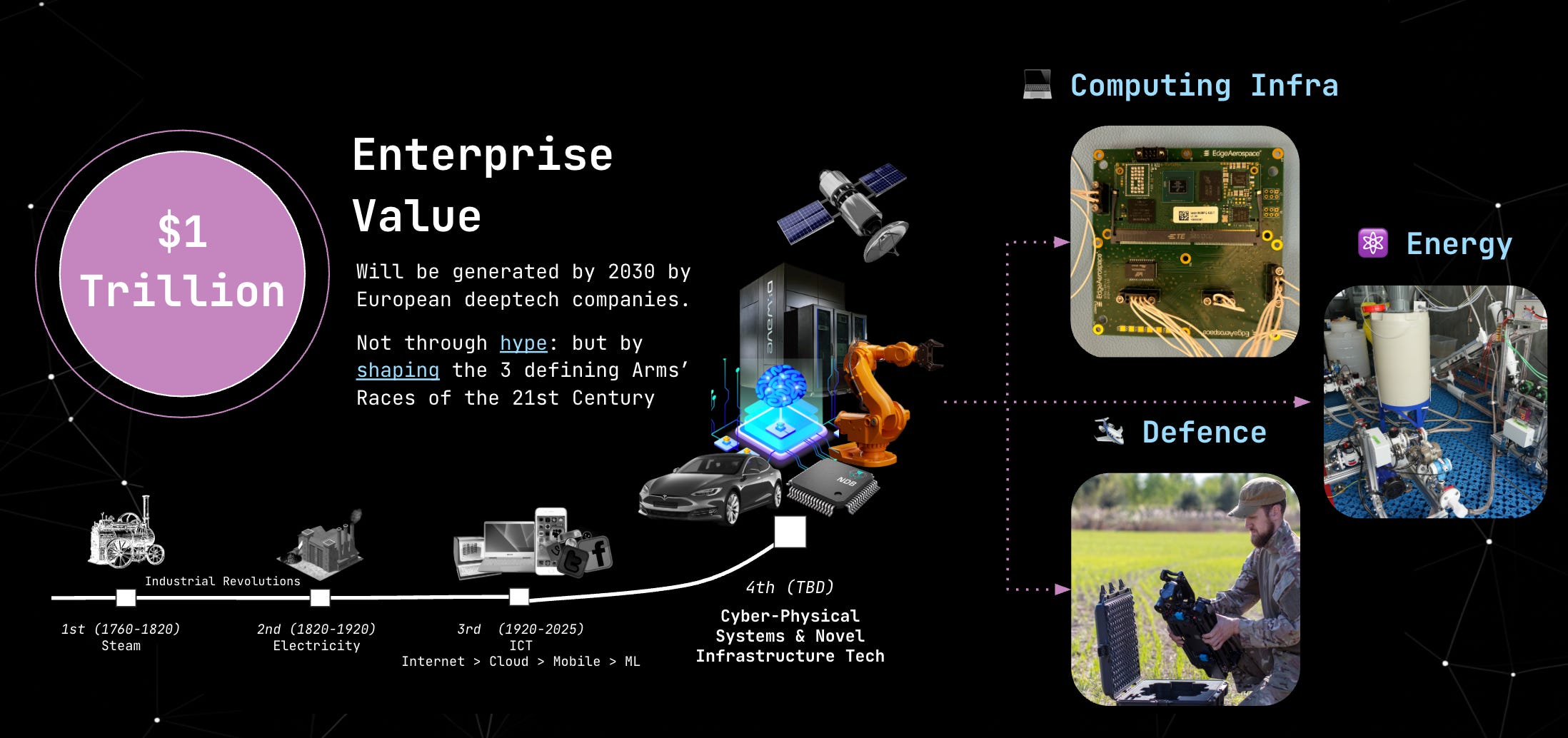

Sovereign Industrialisation: The 2026 Deep Tech Inflection

The end of 2025 and this first quarter of 2026 have confirmed a fundamental shift in the deeptech ecosystem: we have moved from the Discovery Phase to the Execution & Sovereignty Phase.

With just 1 fund vintage we saw defence move from being a “bold gamble” (LPs advised us to take off our deck in 2022-23) to a true propeller (as we predicted) for deeptech, manufacturing and resilience technologies in Europe.

The Opportunity: We are already seeing the birth of European contenders to the US’s Andurils and Palantirs. The strongest of these got started or trace their origins to before the recent hype. Tekever in Portgual is the most obvious example as a unicorn from this category that was founded in 2001. The Filter: We remain disciplined. While the market is currently starting to show sign of over-excitement, with AI-washed drone startups lacking technical moats going from launch to mega-rounds in months, our focus remains on the underlying infrastructure layer - companies with fundamental IP and integrated supply chains.

From Lab to NATO-Standard: For our early portfolio, 2023–2024 was defined by technical breakthroughs in the lab. The end of 2025 and now 2026, instead, are being defined by industrial scale-up and geopolitical hardening. Just as we ignored conservative feedback and moved early into defence because of the de-globalisation and technology trends we could see develop over the last decade, we will continue to choose long-term infrastructure bets over guessing what is or may become hot.

We believer patience will serve us and out LPs well. In the resilience and defence space, both dual use and defence proper players in our portfolio ultimately leveraged the same shift we spotted as investor to take deeptech breakthroughs to market faster. For instance:

Nu Quantum: Secured a world-record Series A for Quantum Networking following national security linked funding.

Origin Robotics: Scaled from prototype to active procurement contracts with several NATO governments in under 18 months.

Yet, we see this search for sovereignty from both investors and institutions play out at different level across our portfolio.

1. The Quantum Networking Inflection

We are seeing the “Quantum Winter” narrative thoroughly debunked. The focus has shifted from “Who has the most qubits?” to “How do we connect them?”

Market Context: Global investment in quantum has crossed $50B, with a massive tilt toward distributed architectures.

Portfolio Zoom: Nu Quantum’s expansion into Spain and their new Cambridge lab positions them as the “Cisco of the Quantum age.” By moving from theoretical networking to industrial-grade Photonic Integrated Circuits (PICs), they are solving the scaling bottleneck that has plagued the industry. Complementing this, Haiqu is drastically lowering the barrier to entry with their hardware-aware OS, targeting a 1000x reduction in compute costs. Essential as the market moves toward Quantum-as-a-Service.

2. The Rise of Sovereign Defence

Autonomous systems are no longer just emerging, they are the new baseline for national security.

Market Context: The autonomous drone segment is seeing a 15.8% CAGR, driven by a shift from hobbyist-grade tech to NATO-codified systems.

Portfolio Zoom: Origin Robotics’ delivery of the BLAZE interceptor to Latvia, Estonia, and Belgium is a landmark moment. Being the first NATO-codified autonomous interceptor gives them a first-mover moat that is incredibly difficult for newcomers to bridge. Simultaneously, Archangel Lightworks is providing the un-jammable backbone for this new era. Their partnership with Eutelsat OneWeb proves that laser-based (optical) communication a viable path for secure, high-capacity global LEO networks.

3. AI’s Energy & Security Crisis

As AI models grow, the traditional silicon and software-only security approaches are hitting a wall.

Market Context: The EU Cyber Resilience Act (CRA) milestones in 2026 are forcing a rethink of hardware security.

Portfolio Zoom: SCI Semiconductor is perfectly timed here. By delivering memory-safe (CHERI-enabled) microcontrollers, they are selling more than a chip - they offer compliance and resilience for critical national infrastructure. On the efficiency side, Finchetto is addressing the AI power wall. Their all-optical switching technology is no longer a luxury, but it is becoming a necessity for data centres that are otherwise reaching the limits of their local power grids.

4. Industrial Scale-Up & Hyper-Mobility

Deep tech is finally touching heavy atoms—iron and infrastructure.

Market Context: The race for Green Iron and sustainable supply chains is drawing massive capital toward industrial automation and regional mini-mills.

Portfolio Zoom: Sparkmate‘s transition to a Stage 1 factory with full process automation is a masterclass in de-risking. Achieving 3N purity iron in a single step undercuts traditional carbon-intensive methods. Meanwhile, Swisspod continues to lead the Hyperloop realisation phase, proving that high-speed, zero-emission cargo transit is a matter of when, not if, as they move from record-breaking missions to site-specific feasibility.

GP Perspective: Why 8 companies breaking above $1m in annual revenue is the Foundation

Our current Fund 1 performance reflects a portfolio that has matured through one of the toughest fundraising environments in a decade. We are seeing a flight to quality where companies with real revenue and industrial contracts (Origin, Astral, Ephos) are separating from the pack.

The fact that Ephos secured the first-ever EU Chips Act startup funding and Origin is actively delivering to three NATO nations, both in the nearly 40% of our 21 bets to date that broke above the symbolic $1m annual revenue, suggests that resilience, just like other trends we’ve been following for many years, are accelerating the path to market for deeptech / hardware entrepreneurs.

With 70% of our portfolio having already raised US capital (and therefore unlocking global funding for scale), we believe the long term trajectory for these deeptech infrastructure champions is one that points up and to the right. It will take longer than AI software plays. But, once again, we don’t believe venture capital to be an investment field you can rush.

LP Only Section Begins